By Drew Hefflefinger, CFP®

The ability to generate income is typically a young professional’s greatest financial asset. To keep life afloat today and build for the future requires regular incoming cash flow. To break this down there are two primary themes to consider — what you can, and cannot control.

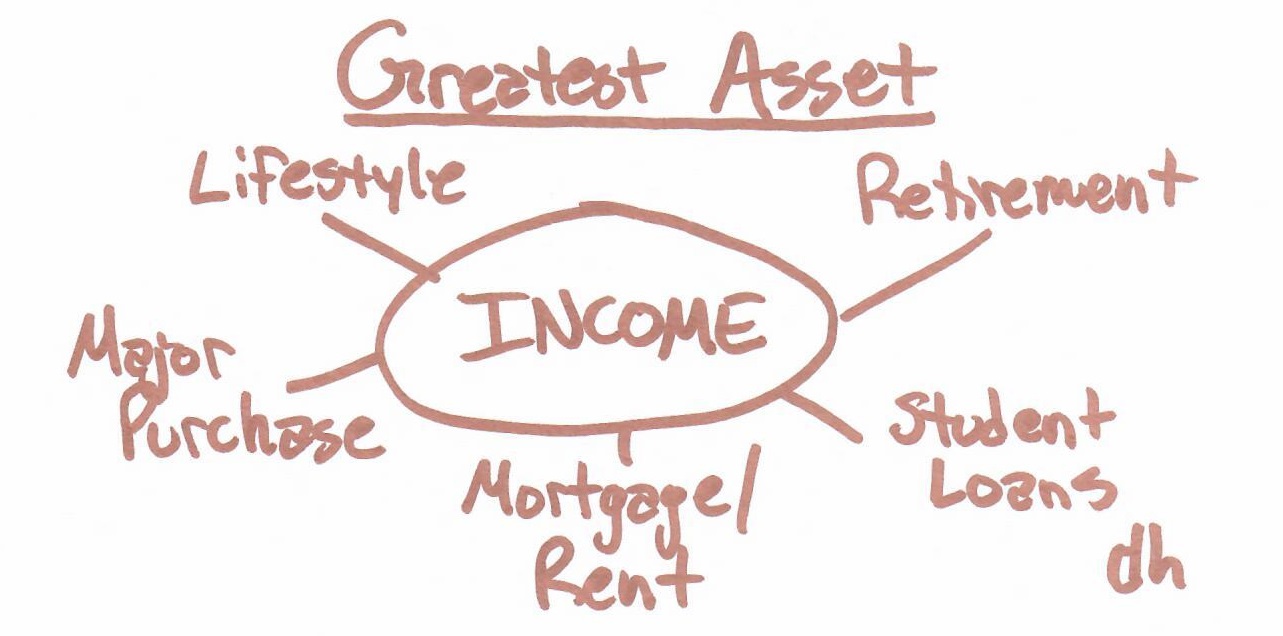

What is your greatest financial asset? To many it stumps — from homeowners I often hear, “my home”. However, this is not true in many cases, often home equity (market value – liabilities) is fairly low in early years. To take a step back: How do the bills get paid? How does the mortgage/rent get paid? How does the retirement account get funded? The engine driving these obligations is income.

Focus on what you can control: Education, performance, and professional networks are all important considerations when determining value in the workplace. These characteristics may help keep your job in tough times, grow your income, and/or land your next gig.

Discussed in “Financial Bites: Student Loans [Part One]” education is one of the single biggest drivers of income. An advanced degree holder can expect to earn about $1.5 million dollars more than the bachelor’s degree holder over the course of their career. What is also important, bachelors and advanced degree holders have a significantly lower unemployment rate than others. Bottom line: knowledge is power AND security.

Beyond schooling we can grow value though workplace performance. One of my early mentors always told me, “get comfortable being uncomfortable by doing what others are not willing to do — by doing so you become rare, and people like to buy rare things”. Although this is easily applied to the penthouse downtown, the same concept applies to an individual’s skill set, just look at the career of Steve Jobs and his development of the iPhone — it stood out and Apple is now one of the most valuable companies in the world.

In and out of the workplace make your brand heard. Being well connected not only increases the opportunity to acquire valuable new business, but as odd as it may sound, being connected is a form of income risk management. How did you get your job today? Was it through a job board, or someone you know? Beyond entry-level roles many sought after jobs are discovered and landed through engaging personal networks.

Diversify and transfer risks you cannot control: The economy, employers, death, and disability are all beyond our reach and we never quite know when they will, if ever, turn against us. Part of protecting income is considering the negative effects of these possibilities.

In the case of the economy and our employers we do not know when the next wave of layoffs will occur. Looking back on the 2008 financial crisis millions of skillful and hardworking people lost their jobs as the economy shrank and employers struggled to maintain the bottom-line. Whether cuts are economy-wide, industry specific, or even company specific — having emergency reserves and a strong network will soften the impact and get you back on your feet faster.

Considering the possibility of pre-mature death and disability is never easy, but vital to protecting individual and family income. If you are single and have no dependents the concern over how death will affect your finances is mostly null and void. However, the possibility of disability, either temporary or permanent, is very real and largely out of control. Disability can take many forms… I can ski off a cliff in Breckenridge and risk severe and lasting head trauma… but I chose to do that. What is more worrisome is degenerative diseases. In the past I worked with a former anesthesiologist who at 40 years old developed a form of multiple sclerosis that left him unable to practice medicine. He was unable to provide for his family on his own, but wisely transferred the risk of disability to an insurance company at an earlier age. Today he is still able to provide for his family through his insurance benefits despite being out of the workforce.

In the case of pre-mature death, we cannot control when this will occur. Most of us will live long and healthy lives given we take care of ourselves, however, the world acts in odd ways. To protect family income we can transfer the risk of death to an insurance company. Essentially taking a near bottomless pit of possible financial hardship and giving it to someone else at a relatively low cost. Coupled with disability coverage, life insurance is a core strategy and should be considered in all family risk management plans.

Overtime a majority of readers will become financially independent and no longer worry about generating a formal income — to many this is called retirement. To reach this goal it is important to save and build a nest egg that is sustainable for a lifetime. Doing so requires discipline, sound investment behavior, and personalized strategy.

Drew Hefflefinger is a CERTIFIED FINANCIAL PLANNER™ at Private Client Wealth Advisors, LLC in Denver, Colorado. Drew specializes in working with young professionals by helping them preserve and grow their wealth while achieving life goals. Drew can be contacted at drew@pc-wa.com.

{kind=link}

{kind=link}

Leave A Comment